9 Steps to Financial Freedom (Take Control of Your Money)

Financial freedom is not just a dream. It's a process. And like any process, it follows a cycle. If you want to escape the pay check-to-pay check grind or retire early, you need to understand and apply a proven approach. Let's be honest: financial problems can be challenging to manage. But what if you're already on the right path to financial freedom and don't even realize it?

Meet Sam, a mid-level professional who manages to balance work, expenses, and the occasional impulse purchase. His car broke down one morning. He didn't freak out; instead, he looked at his budget, moved some money around, and paid for the repair without missing rent, borrowing money, or worrying about it. That calm response? Clear evidence of financial strength.

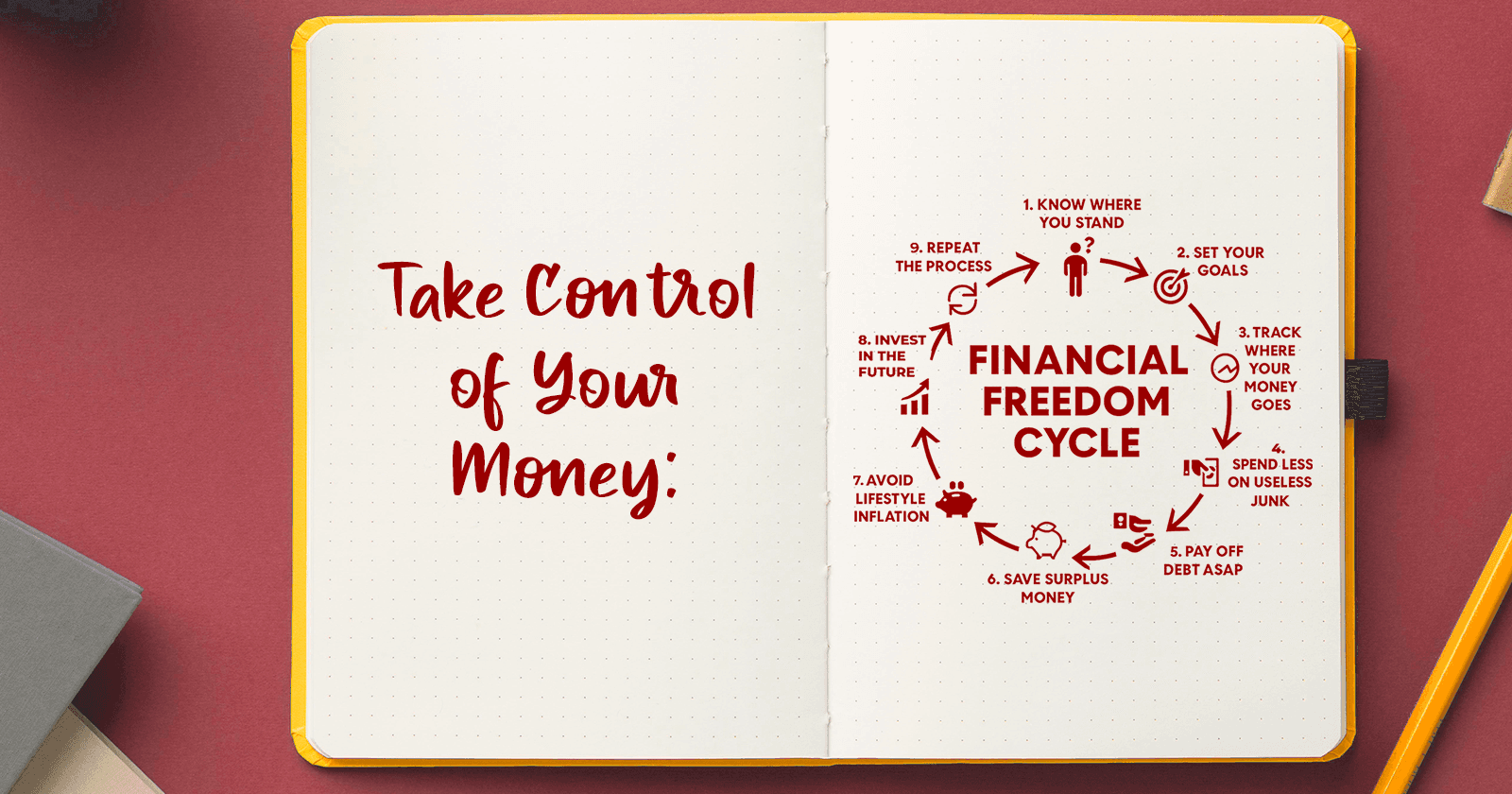

Here are 9 simple yet powerful steps in the Financial Freedom Cycle that allow you to take control of your money:

- Know Where You Stand

You need to know exactly where you stand financially before you can improve your situation. That entails writing down all of your income, keeping track of your monthly expenses, and determining how much you owe and own, including your bank accounts, investments, loans, and credit cards.

This method of creating a personal balance sheet is akin to taking a snapshot of your finances. Monitoring your net worth (assets minus liabilities) is an essential metric for assessing your financial well-being, as it provides a level of insight that surpasses mere awareness of your salary or monthly expenses.

Researchers have found that regularly reviewing your net worth can help you spend less, set more effective goals, and pay off debt. One Moneycontrol article, for example, says that keeping track of your net worth "helps set realistic goals" and encourages you by showing how much you've improved over time. Net-worth tracking tools or spreadsheets updated monthly or quarterly enable you to spot trends. If assets rise and liabilities fall, you're moving forward. If not, you can identify the issue early.

Action Tip: Begin with a simple spreadsheet or use an app to record every asset and liability. Revisit it regularly. Your calm, informed financial decisions depend on this foundation.

- Set Your Goals

What does financial freedom mean to you? Is it owning a home, retiring early, clearing all your debts, or starting a business? Whatever it is, clarity is your greatest asset.

The key is to set SMART goals: Specific, Measurable, Achievable, Relevant, and Time-bound. For example, instead of saying, "I want to save more," say, "I want to save KES 50,000 in the next 6 months for an emergency fund." This not only provides direction but also fosters a sense of purpose.

Research has consistently shown that people who set specific financial goals are more likely to change their behavior and make progress. A study by the Dominican University of California found that individuals who write down their goals and share them with a friend are 33% more likely to achieve them.

Goal-setting also activates the brain's reward system. When you hit small milestones (like paying off one loan), your brain releases dopamine, which builds momentum and keeps you motivated.

Action Tip: Write down three financial goals right now: one short-term (1–6 months), one mid-term (1–5 years), and one long-term (5+ years). Ensure they follow the SMART format and review them monthly.

- Track Where Your Money Goes

You can't control what you don't measure. That's why tracking your spending is one of the most powerful tools in your financial freedom journey.

When you monitor where every shilling goes, whether it's rent, airtime, Uber rides, or snacks, you begin to notice patterns. You may be spending more on delivery than you thought. Perhaps your daily coffee habit adds up to thousands of dollars a month. Awareness brings change.

Studies show that individuals who consistently track their expenses are more likely to adhere to their budgets and achieve their savings goals. Behavioral economists refer to this phenomenon as the "observation effect"; simply observing your behavior can have a positive influence on it.

Research has found that tracking expenses can reduce unnecessary purchases by up to 20%. It encourages you to pause before you spend and ask, "Is this aligned with my goals?"

Even basic tools, such as a notebook, an Excel sheet, or free budgeting apps, can help. Over time, you'll begin to identify what to cut, where to make adjustments, and how much you can save or invest.

Action Tip: For the next 30 days, record every expense, no matter how small. At the end of the month, review your list and highlight anything you could reduce or eliminate.

- Spend Less on Useless Junk

Let's be honest: most of us spend money on things we don't need. It might be daily takeout, multiple subscriptions you barely use, or impulse buys triggered by TikTok trends and flash sales.

This type of spending is called discretionary spending money, which isn't essential for survival. While small in the moment, it adds up quickly. Skipping just one KES 400 lunch four times a week could save you over KES 80,000 in a year.

Behavioral psychology explains this using the concept of "mental accounting." we treat some money (like bonuses or refunds) as easier to spend wastefully. Another factor is "the pain of paying." When we use cash or mobile money and see the money leave instantly, we're more aware. This awareness helps reduce unnecessary spending.

A study by researchers at MIT and Stanford found that people spend more when using cards or digital payments because they feel less emotional impact compared to paying with cash.

Cutting junk spending doesn't mean cutting joy. It means spending with intention.

Action Tip: Review your expenses from last month. Highlight any purchase that didn't bring lasting value. Commit to skipping at least one unnecessary item this week and redirect that money to savings or debt.

- Pay Off Debt ASAP

Debt is one of the most significant barriers to achieving financial freedom. Prioritizing debt repayment not only reduces your financial stress but also frees up cash flow that can be redirected toward savings and investments.

Experts recommend focusing on paying off loans quickly to avoid accumulating more debt, which can often become a burden. According to a 2020 study by the Federal Reserve, Americans with high credit card debt have significantly lower savings rates and face greater financial insecurity. This highlights the importance of eliminating debt as soon as possible.

Two popular methods for tackling debt are the Snowball Method, which pays off the smallest balances first to build momentum, and the Avalanche Method, which focuses on debts with the highest interest rates to minimize overall costs. Both have proven effective, but the key is consistent payment and avoiding new borrowing.

Accumulating loans, especially consumer debt, traps many individuals in a cycle of repayment and interest, making it harder for them to progress financially. As CNBC reports, paying off debt early can save thousands in interest and accelerate your journey to financial independence.

Action Tip: List all your debts, prioritize paying them off by starting with either the smallest balance or the one with the highest interest rate, and avoid taking on new loans unless necessary.

- Save Surplus Money

Once you've successfully cut expenses and reduced your debt, you'll likely find yourself with surplus money each month. This extra cash is a powerful tool — but only if you use it wisely. Rather than letting it sit idle in a checking account, channel it into building an emergency fund and consistent savings.

An emergency fund acts as a financial safety net, protecting you from unexpected expenses like medical bills, car repairs, or sudden job loss. Financial experts propose that you should keep at least three to six months' worth of living costs in an account that is easy to get to. Bankrate's 2022 study found that only 39% of Americans have enough savings to handle a $1,000 emergency. This illustrates the importance of this cushion at present.

Making your savings automatic makes the process easy and regular. People who automate their savings are more likely to attain their financial objectives because it makes them less tempted to spend money. The University of Illinois conducted research that revealed automatic transfers to savings accounts increased the total rate of saving by 30%.

Having a surplus savings fund not only gives you peace of mind but also gives you a place to invest and grow your wealth. It ensures you won't need to rely on loans or credit when emergencies strike, keeping you on track toward financial freedom.

Action Tip: Set up an automatic monthly transfer to a separate savings account dedicated to emergencies, starting with a small amount and increasing over time.

- Avoid Lifestyle Inflation

As your income grows, it's natural to want to upgrade your lifestyle. But if you fall into the trap of lifestyle inflation, which means spending more as you earn more, it can make it much harder to get to financial freedom. Instead of spending more money, focus on saving and investing more while keeping your living costs low.

Studies consistently indicate that lifestyle inflation is one of the primary reasons many people struggle to build wealth despite increasing salaries. The Federal Reserve conducted research that showed that even as average salaries increased significantly over the years, household spending also rose, leaving little additional money for saving or investing. Financial experts say that real wealth comes from what you maintain, not just what you make. For instance, a 2021 Fidelity Investments analysis found that higher savings rates, not just better income, were the best indicator of long-term financial security.

To combat lifestyle inflation, try increasing your savings rate whenever you get a raise or bonus, and aim to save at least 50% of any additional income. Keep living costs stable by avoiding unnecessary upgrades, such as expensive cars, larger homes, or luxury gadgets, which can drain your surplus.

Action Tip: Commit to saving or investing a fixed percentage of all income increases. Celebrate financial wins by growing your net worth, not by spending more

- Invest in the Future

Saving money is essential, but investing it wisely is what truly accelerates your journey to financial freedom. You can get compound interest by putting your money to work in stocks, mutual funds, retirement accounts, or real estate. This means you get interest on both your original investment and the money it makes over time.

The earlier you start investing, the more your money can grow because of the power of compounding. Research by Nobel Prize winner Robert Shiller, a well-known figure, found that investing continuously over decades is more effective than simply saving.

For Kenyans, accessible platforms like the Nairobi Securities Exchange (NSE) enable investment in local stocks and bonds. Some mobile apps provide easy access to both local and international markets, including U.S. stocks and ETFs, with low fees and user-friendly interfaces.

Globally, platforms such as Vanguard, Fidelity, and Charles Schwab offer broad access to mutual funds and retirement accounts, including IRAs and 401(k)s, which are ideal for long-term growth. Real estate investment trusts (REITs) are another option that offers exposure to property markets without needing large capital.

Action Tip: Open an investment account today, even with a small amount. Automate monthly contributions to build wealth steadily over time.

- Repeat the Process

Financial freedom isn't a one-time achievement—it's an ongoing cycle. Life circumstances, goals, and financial markets change, so your financial plan must evolve, too. Regularly reassessing your goals, reviewing your budget, and refining your strategies keeps you on track and responsive to new challenges and opportunities.

Studies show that individuals who consistently review their finances are more likely to adhere to budgets and achieve their financial objectives. For example, a 2021 survey by Northwestern Mutual found that 62% of financially successful individuals review their budgets monthly, while only 28% of those struggling financially do the same.

By revisiting your financial snapshot, you can identify shifts, such as changes in income, unexpected expenses, or new debts. This enables you to adjust spending, savings, and investment plans proactively rather than reactively. Furthermore, revisiting goals keeps your motivation alive; a 2015 study by Dominican University revealed that writing down and regularly reviewing goals increases the likelihood of achieving them by 33%.

Financial freedom is a dynamic journey what works today might need tweaking tomorrow. Make it a habit to reflect at least twice a year or quarterly if possible. This adaptive mindset is key to building lasting wealth and resilience against financial setbacks.

Action Tip: Schedule regular financial check-ins on your calendar and treat them like essential appointments.

The Financial Freedom Cycle isn't a quick fix; it's a long-term solution. If you follow these nine stages, you'll establish a strong foundation that'll help you reach your financial goals, no matter what life throws your way. The most important thing is to start small, choose one step that you can do today, and stick with it. Keep in mind that financial freedom isn't about being rich quickly; it's about making continuous progress through smart decisions. Every little thing you do, such as keeping track of your expenditures, paying off debt, or putting a bit extra money into investments, adds up over time and helps make your dreams come true. Are you ready to stop thinking about money and start living the life you want? One step is all it takes to start on the road to financial freedom. Do that thing today, and your future will change.